I am getting a lot of questions from my clients about the effect of the proposed tax bill. The bill, known as the Tax Cuts and Jobs Act, proposes significant changes for both individuals and businesses. This will be the first significant overhaul of the U.S. tax code in more than 30 years. The goal of the change is to provide tax relief for individuals and businesses by cutting and simplifying taxes.

The law is not finalized now and a lot can change, but people want to know what could happen. Here is a quick synopsis of the plan.

Individual Provisions

The major change proposed is the elimination of a number of itemized deductions and credits countered by a lower overall tax rates and increased basic deductions.

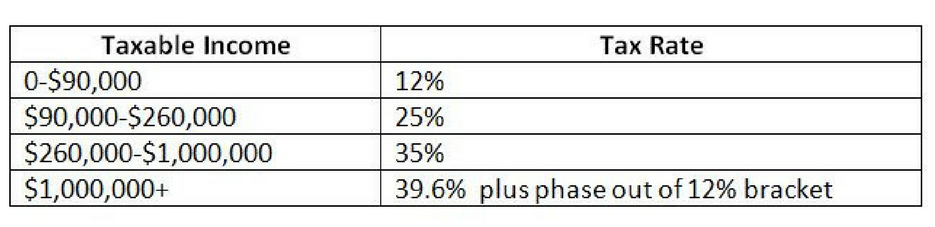

- Reduction in the Number of Tax Brackets – Married Filing Jointly (MFJ) Tax Rates (Single = ½)

- Standard deduction increased to $24,400 MFJ

- Personal exemptions are eliminated

- 25% tax rate on business income of individuals

- Complicated formula

- Applies to passive activities 100%

- 30% of active business income will be taxed at 25% the remainder at the normal rate (if higher)

- 25% tax rate does not apply to personal service companies

- Child tax credit increased to $1,600 phase out starts at $230,000 for MFJ

- All three education credits are combined into American Opportunity Tax Credit

- Same calculation

- Available for the 5th year at reduced level (50%)

- Up to $10,000 a year is able to be distributed from a 529 plan to pay for grade school and high school tuition

- No student loan interest deduction

- Above the line qualified tuition expense is gone

- US Bond exclusion for education expenses is gone

- Employer provided education assistance is repealed

- 3% phase out of itemized deductions is repealed

- New mortgage loan limits will be $500,000. Only interest from one house is deductible (not sure about home equity)

- Real estate taxes are limited to $10,000

- State and local (including personal property etc.) tax deduction is repealed

- Medical expenses, 2106 expenses, tax prep fees, casualty loss (except disaster zones), moving expenses are no longer deductible

- No deduction for alimony

- Need to use the residence five of the past eight years to exclude gain on sale of home. Phase-out for high income taxpayers (not specified)

- Dependent care exclusion from income is repealed.

- Estate tax exemption is doubled to $10M and repealed starting in 2024. (Don’t count on that)

- Alternative Minimum Tax (AMT) is repealed

Business Tax Changes:

- Flat corporate tax rate of 20%. Personal service corps are 25%

- Immediate expensing of all personal property (and land improvements?) starting 9/27/17 through 12/31/2022. No limits. Available on new and used property

- Section 179 is increased to $5,000,000 with phase-out at $20,000,000

- Increase use of cash method for taxpayers with less than $25,000,000 of receipts

- Interest expense will be limited for companies with more than $25,000,000 in receipts. Complicated formula.

- Net Operating Losses (NOL) will be limited to 90% deduction each year. Similar to current AMT NOL rules.

- Carrybacks limited to one year for small businesses. (Probably less than $25,000,000)

- AMT is repealed.

- Like kind exchanges limited to real property. Does not apply to personal property.

- No deduction allowed for entertainment. The 50% limitation will apply only to business meals.

- Sale of self-created intangibles will be taxed at ordinary rates.

- No Domestic Production Activities Deduction

- Most credits are eliminated. (R&D and Low income housing stay)

- Orphan drug

- Employer child care credit

- Rehab credit

- Work opportunity credit

- New Markets tax credit

- Limits on compensation and changes to deferred comp rules

What’s Next?

The full bill is available here but the Tax Cuts and Jobs Act – H.R. 1 – Section-by-Section Summary from the Ways and Means Committee explains each change in a way that’s easier to comprehend.

All the proposed changes will be effective for the 2018 tax year with the expectation of the immediate expensing of property, which would be effective 9/27/2017. As more details emerge, it’s important to understand how your taxes will be affected by these changes. Please contact the tax department with any urgent questions regarding the outlined changes.